Bacaan teman ngopi Anda sore ini. Semoga bermanfaat!

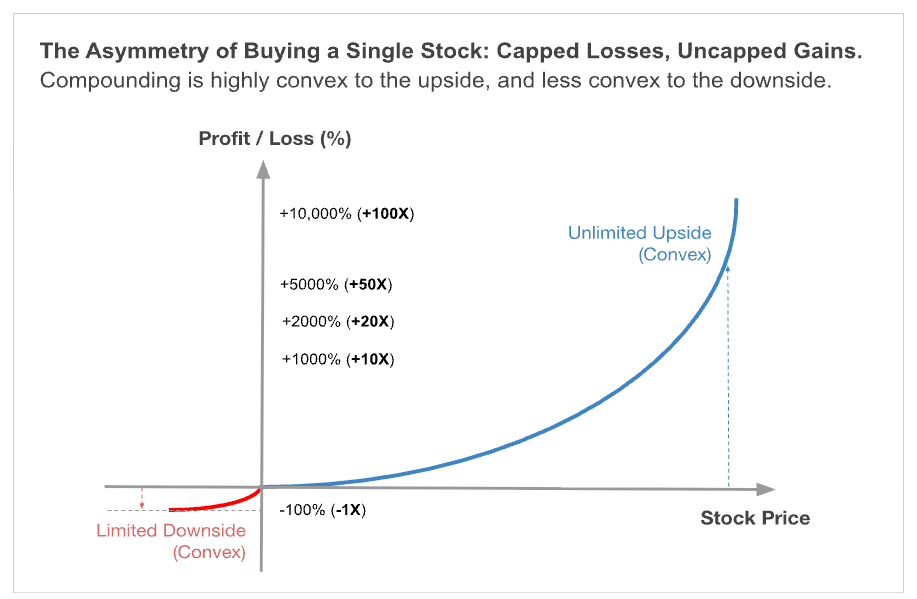

Asymmetry is the holy grail in finance. The initial return profile of buying a stock is symmetrical. If a stock goes up 25%, you make 25%, and vice versa, if a stock goes down 25%, you lose 25%.

Yet over the long term, it is certainly not symmetrical. The risk-reward asymmetry becomes compelling. When buying a stock, the downside is capped at 100%, but the upside is theoretically unlimited, with potential returns of 10x, 20x, or 50x. Each long stock position functions like a long call option, and a portfolio of stocks effectively resembles a giant long call option payoff.

Asymmetry is the holy grail in investing, where over a long time, in heads, you don’t lose a lot, and in tails, you win increasingly more.

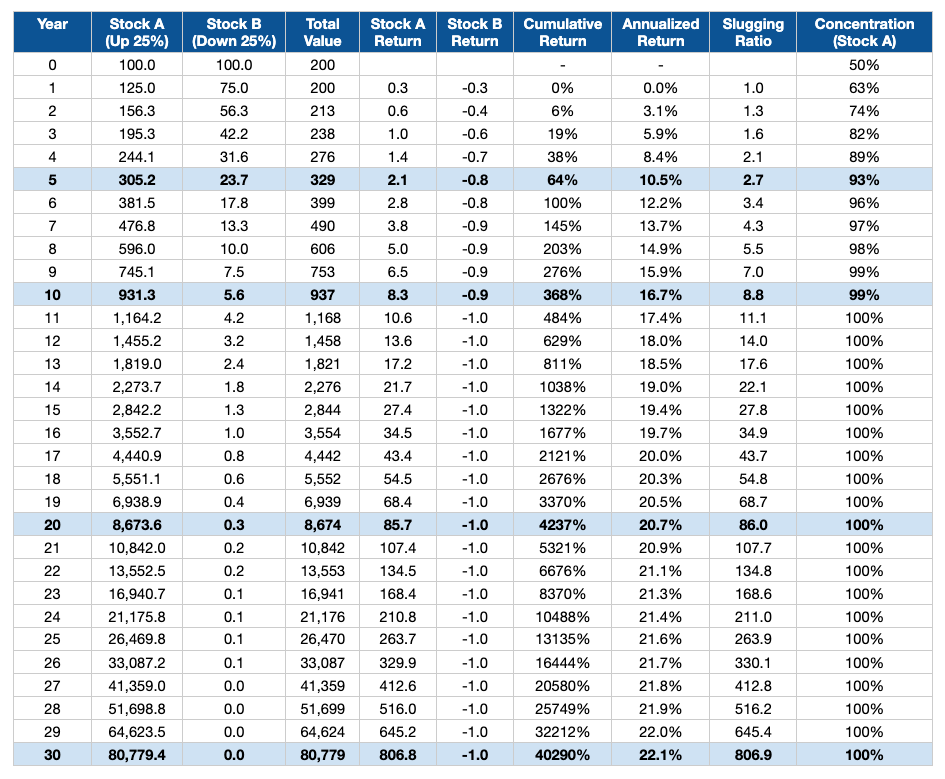

Let’s start with 100 equally invested in Stock A and B. The price of Stock A keeps rising 25% every year, and Stock B keeps declining 25% every year. (shown in picture 1 below)

In the first year, the value of Stock A rises 25% to 125, and Stock B declines 25% to 75. The portfolio value remains unchanged at 200 with 0% returns (not good).

At the end of year 5, Stock A rose ~3X to 305, and Stock B has declined by 76% to 24. The portfolio value is 329, with a cumulative return of 64% and an annualized return of 10.5% p.a. (good).

At the end of year 10, Stock A rose ~9.3X to 931, and Stock B has declined 94% to 6. The portfolio value is 937, with a cumulative return of 368% and an annualized return of 16.7% p.a. (strong).

At the end of year 20, Stock A is an 86-bagger to 8674, and Stock B has declined 99.7% to 0.30. The portfolio value is 8,674, with a cumulative return of 4237% and an annualized return of 20.7% p.a. (very strong).

While we acknowledge that the assumptions are highly simplistic:

(1) a constant 50% batting average

(2) an equal-weighted two-stock portfolio

(3) both stocks rising and declining at the same rate,

the following lessons are instructive.

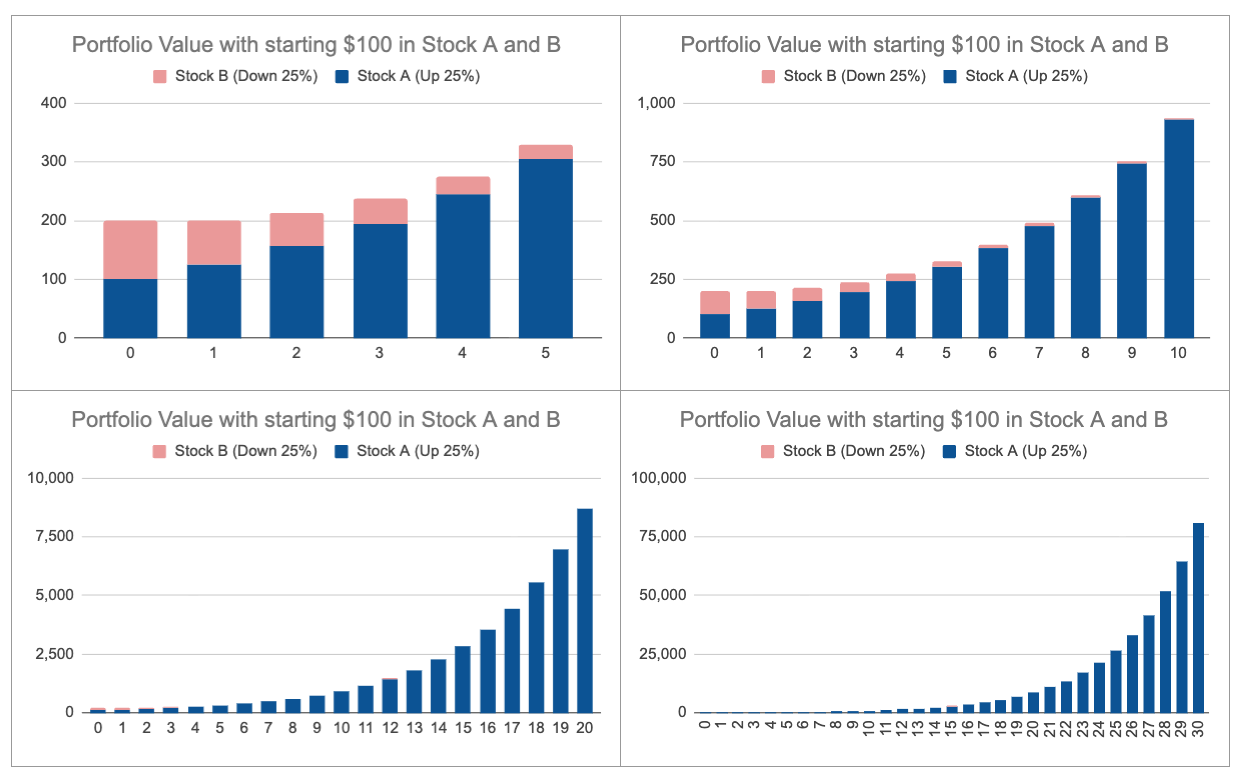

*𝐖𝐢𝐧𝐧𝐞𝐫𝐬 𝐢𝐧𝐜𝐫𝐞𝐚𝐬𝐢𝐧𝐠𝐥𝐲 𝐦𝐚𝐭𝐭𝐞𝐫, 𝐥𝐨𝐬𝐞𝐫𝐬 𝐢𝐧𝐜𝐫𝐞𝐚𝐬𝐢𝐧𝐠𝐥𝐲 𝐝𝐨𝐧’𝐭. If you have a winner, a little is all you need, and even if you do have a loser, it doesn’t matter. Asymmetry does not exist in discrete time periods, but shows up over time. (as illustrated in picture 2)

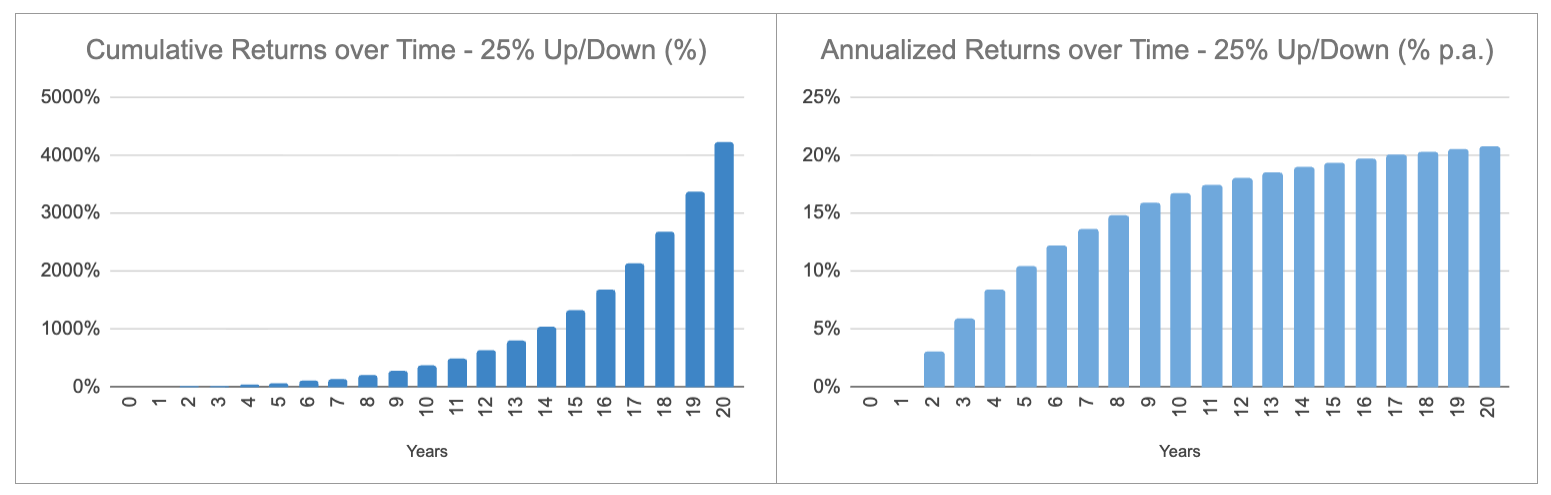

*𝐂𝐨𝐦𝐩𝐨𝐮𝐧𝐝𝐢𝐧𝐠 𝐬𝐭𝐚𝐫𝐭𝐬 𝐬𝐥𝐨𝐰 𝐛𝐮𝐭 𝐚𝐜𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐞𝐬 𝐨𝐯𝐞𝐫 𝐭𝐢𝐦𝐞. Returns take time to show up, only if the winners are held. Being able to hold on to winners and not trim them allows one to keep growing cumulative returns exponentially and annualized returns towards steady-state rates of 20%-22%+ p.a. after 10-20 years. (as illustrated in picture 3)

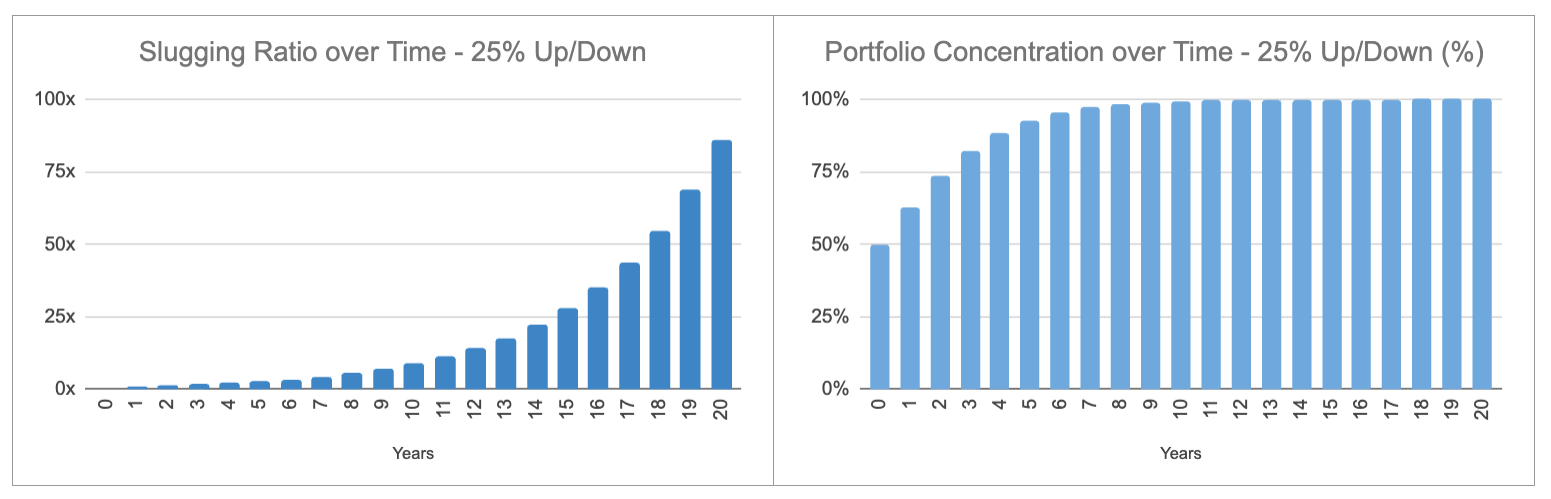

*𝐖𝐢𝐧𝐧𝐞𝐫𝐬 𝐛𝐞𝐜𝐨𝐦𝐞 𝐢𝐧𝐜𝐫𝐞𝐚𝐬𝐢𝐧𝐠𝐥𝐲 𝐬𝐢𝐠𝐧𝐢𝐟𝐢𝐜𝐚𝐧𝐭 𝐚𝐬 𝐲𝐨𝐮 𝐡𝐢𝐭 𝐢𝐭 𝐨𝐮𝐭 𝐨𝐟 𝐭𝐡𝐞 𝐩𝐚𝐫𝐤, 𝐚𝐬 𝐩𝐨𝐫𝐭𝐟𝐨𝐥𝐢𝐨 𝐜𝐨𝐧𝐜𝐞𝐧𝐭𝐫𝐚𝐭𝐢𝐨𝐧 𝐠𝐫𝐨𝐰𝐬 𝐨𝐯𝐞𝐫 𝐭𝐢𝐦𝐞. The gains from the multi bagger winners will keep growing, increasingly offsetting the losers’ combined losses many times over. The losers don’t matter. The winners do. (as illustrated in picture 4)

*𝐒𝐮𝐟𝐟𝐢𝐜𝐢𝐞𝐧𝐭 𝐝𝐢𝐯𝐞𝐫𝐬𝐢𝐟𝐢𝐜𝐚𝐭𝐢𝐨𝐧 𝐢𝐬 𝐧𝐞𝐜𝐞𝐬𝐬𝐚𝐫𝐲 𝐭𝐨 𝐚𝐥𝐥𝐨𝐰 𝐟𝐨𝐫 𝐭𝐡𝐢𝐬 𝐭𝐨 𝐛𝐞 𝐚𝐜𝐡𝐢𝐞𝐯𝐞𝐝, 𝐧𝐨𝐭 𝐛𝐞𝐢𝐧𝐠 𝐨𝐯𝐞𝐫𝐥𝐲 𝐜𝐨𝐧𝐜𝐞𝐧𝐭𝐫𝐚𝐭𝐞𝐝 (<𝟏𝟎 𝐬𝐭𝐨𝐜𝐤𝐬) 𝐨𝐫 𝐛𝐞𝐢𝐧𝐠 𝐨𝐯𝐞𝐫𝐥𝐲 𝐝𝐢𝐯𝐞𝐫𝐬𝐢𝐟𝐢𝐞𝐝 (>𝟑𝟎 𝐬𝐭𝐨𝐜𝐤𝐬). If one is overly concentrated, and if a winner becomes overly large or runs into single-position limits, one eventually has to trim the winner. Constantly trimming your flowers, not allowing your winners to run, and watering your weeds are among the worst things one can do. Sufficient diversification by owning more stocks allows one to have a better risk appetite and more patience to hold on to winners, especially when they experience inevitable large price declines along the way.

Compounding increases at an increasing rate on the upside and decreases at a decreasing rate on the downside. That makes it the eighth wonder of the world. Gains grow faster, and losses shrink slower. Those who understand this asymmetry earn it. Those who don’t, pay it. Find winners, hold them, and let time bend the curve in your favor.

$CASS $ADES $TOTL

1/5