Nemu data bagus nih dari KPMG Indonesia, walaupun cuma sampe 1H2024.. Nice work!

Barangkali bisa jadi bahan tambahan untuk analisa saham.

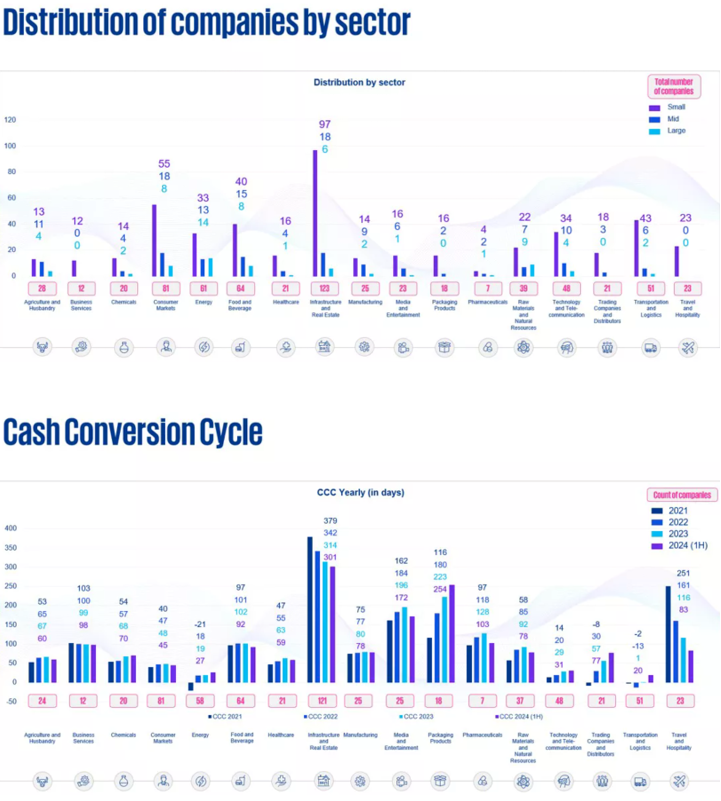

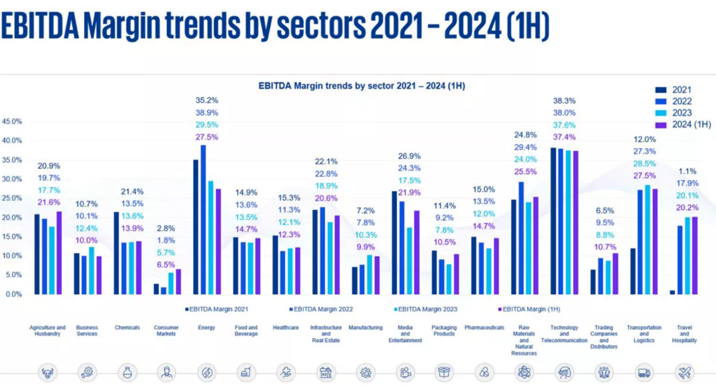

*Population: 780 publicly listed companies across 18 sectors in Indonesia from 2021 to the first half of 2024.

*Working capital performance by company size: Small < USD 200m, Medium USD 200m – USD 1bn and Large > USD 1bn.

*1H 2024 sector performance compared to previous years.

*CCC across the majority of industries has shown improvement, or has at least been stable, since 2021, indicating better cash flow management. However, industries such as product packaging, trading companies and distributors, technology and telecommunications, and energy have shown an increase in CCC, indicating a slowdown in their cash inflow.

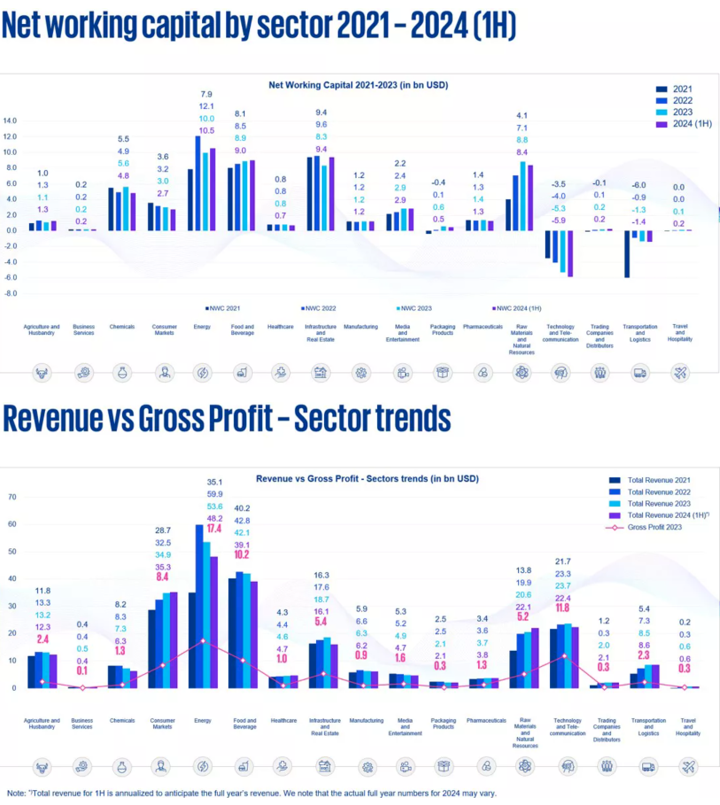

*Declining CCC also aligns with the overall lower NWC levels. However, the raw materials and natural resources sector, as well as transportation and logistics have noticeably greater NWC levels, indicating that they might need to reevaluate their working capital requirements. We also note that the energy industry seemed to be an outlier with significant fluctuations throughout 2021-1H24, likely affected by the change in regulations regarding the transition from coal to renewable energy.

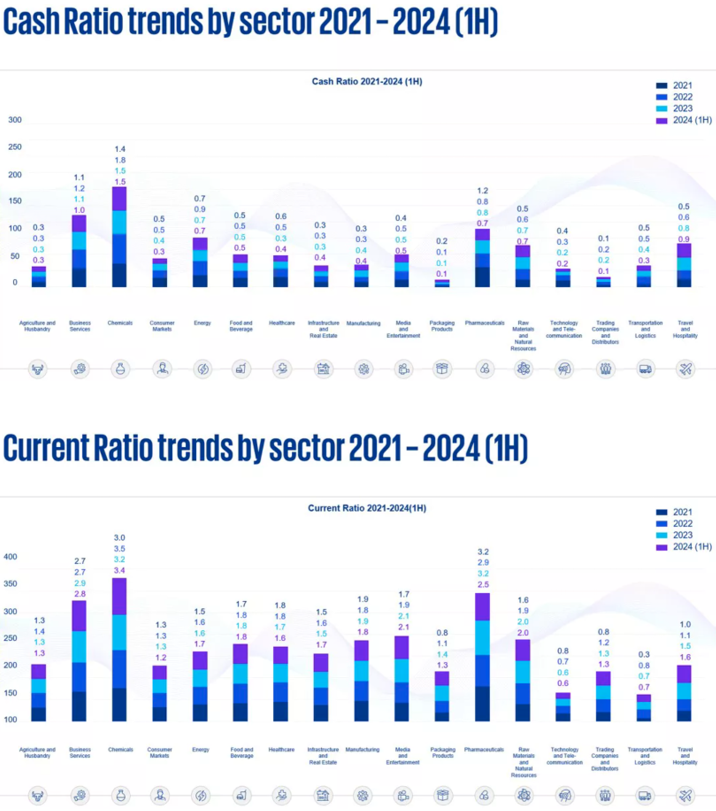

*The cash and current ratios have generally remained steady across the industries, with a couple of notable exceptions. Product packaging as well as transportation and logistics recorded increases in the current ratio which indicates improved liquidity levels, while pharmaceuticals recorded a decrease in the current ratio which might indicate a potential liquidity issue.

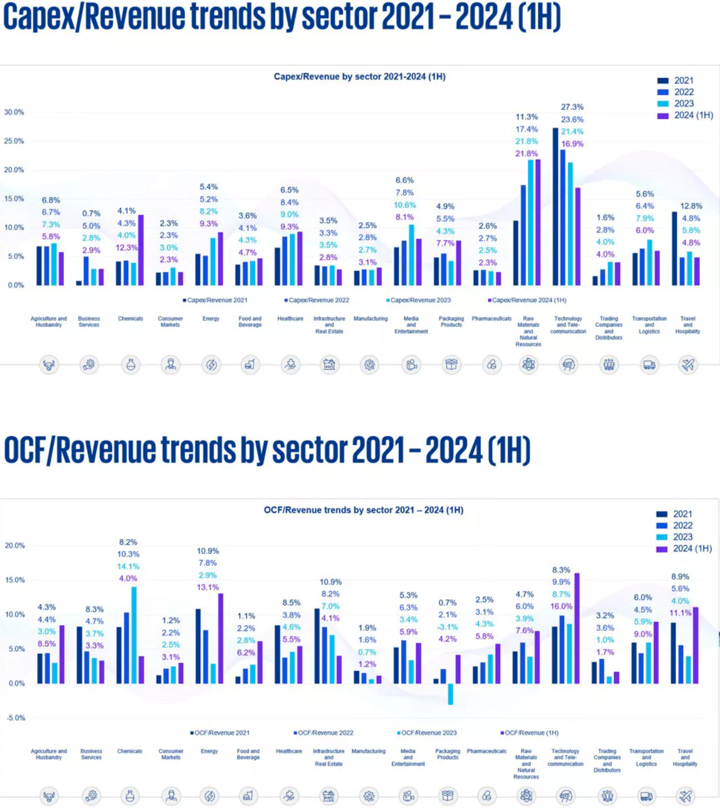

*Capex/revenue generally remained relatively stable. However, there were several outliers that fluctuated significantly, such as raw materials and natural resources as well as technology and telecommunications. Raw materials and natural resources have shown an increasing capex/revenue ratio, indicating that they are investing more in their growth, but their performance has not yet reflected the increased investment. Meanwhile, for technology and telecommunications the capex/revenue ratio decreased.

*EBITDA margins have generally improved, resulting in greater profitability. This is most notable in the travel and hospitality industry, which has recovered drastically after the COVID-19 pandemic. However, the energy industry has shown a decrease in their EBITDA margin.

$BBCA $ASII $TLKM

1/5