$CASS

Let's review the 2Q25 result.

1. Quite impressive growth numbers even though there was trade wars uncertainty in 2Q25. The company recorded +19.6% YoY Revenue growth and +16.32% YoY EBIT Growth when tourist numbers in Indonesia barely grew in 2Q25.

2. -5.7% yoy net profit in 2Q25 due to last year's one-off debt repayment. If we exclude last year's one-off gain, net profit in 2Q25 would be growing more than 20% YoY.

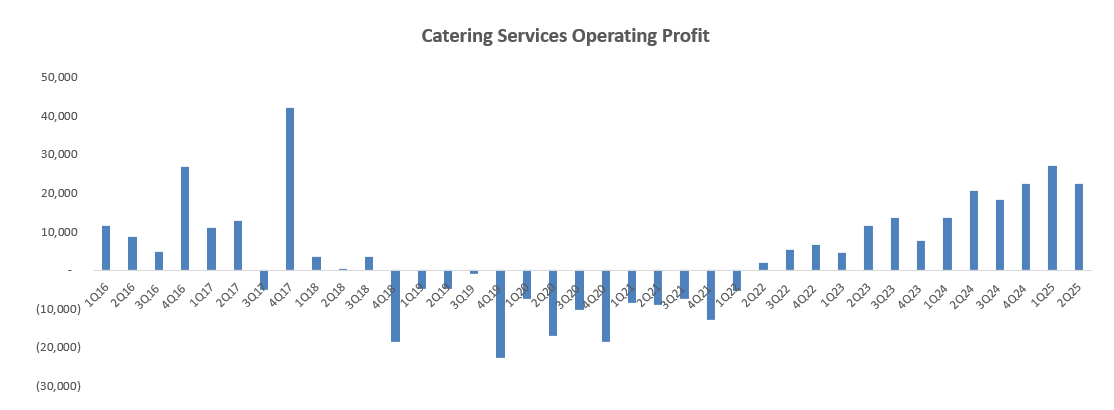

3. What delight me most was that CASS's catering business has been doing very great in the last few years. Catering business has been able to record healthy 16-25% operating margins and impressive 15-60% sales growth in the last few quarters. This was very contrast with catering business pre-covid's financial numbers which was consistently in dire states.

4. In the 3Q25, CASS financial numbers will be burdened by some non-cash one-off items which was: IDR18bn impairment loss from uncollectible receivables from PT JATC, divestment of PT JATC shares for IDR1mn.