Alpha IVF Group Berhad (BURSA: ALPHA): A Deeply Undervalued Regional Growth Story in Fertility Healthcare

Alpha IVF continues to strengthen its regional presence in advanced fertility solutions, backed by resilient margins and an expanding international footprint. At RM0.290 per share, the stock is trading at a significant discount to its fair value of RM0.420, as reaffirmed by AmInvestment Bank. This valuation is based on a 28x price-to-earnings multiple on CY2025 earnings, suggesting considerable upside for investors who recognise the Group’s long-term growth trajectory.

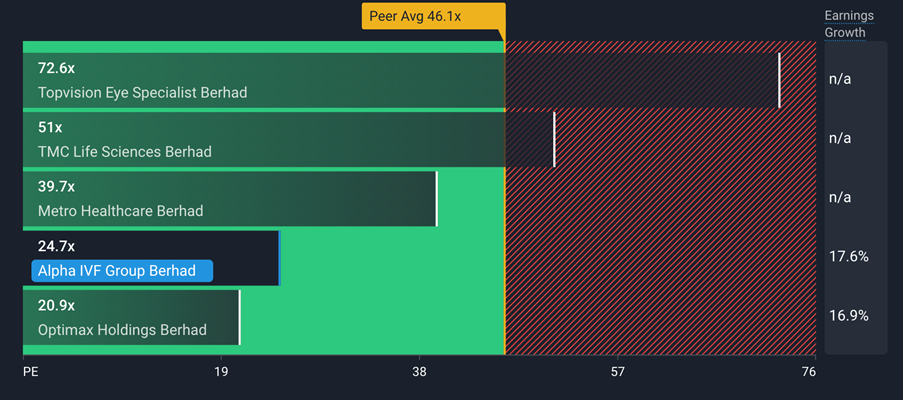

Source: SimplywallSt

For the first quarter of FY2025, Alpha IVF reported a slight dip in revenue and core net profit on a quarter-on-quarter basis, primarily due to the high base effect from 4QFY24. This was anticipated, as festive delays in 3QFY24 had led to a concentration of patient treatments being deferred into the final quarter of FY2024.

Nonetheless, profitability remained intact with the Group recording a commendable gross margin of 59.7%, improving further from FY2024’s 58.1% and FY2023’s 55.7%. This margin strength was largely driven by a sustained contribution from foreign patients, underscoring the Group’s appeal as a cross-border fertility destination.

The number of Oocyte Pick-Up (OPU) procedures in 1QFY25 stood at 770, slightly lower year-on-year and quarter-on-quarter. However, this is not a structural concern. Alpha IVF is actively expanding its medical team with the planned onboarding of a high-profile Obstetrician and Gynaecologist, expected to uplift capacity utilisation from its current implied rate of 38.5%.

In parallel, the Group is preparing to open two new full-fledged IVF centres, one each in FY2025 and FY2026, with Sabah identified as a potential site, which should support capacity growth ahead.

Alpha IVF’s international strategy is also gaining traction. In China, despite the end of the favourable “Dragon baby” conception window, patient volumes remain robust. Revenue from Chinese patients in 1QFY25 came in at RM6.9 million, already exceeding 50% of FY2024’s full-year contribution.

The Group has identified China as a key growth market, leveraging regulatory arbitrage; particularly in areas such as Preimplantation Genetic Testing, which is restricted in China. To enhance market access, Alpha IVF launched its first sales representative office in September 2024 and is preparing to establish a second.

In Southeast Asia, expansion plans are advancing steadily. The Group is finalising land leases for a full-fledged IVF centre in Bali, while planning four satellite clinics across Indonesia, two in FY2025 and another two in FY2026.

The first of these, located in Jakarta, is set to launch by early 2025. Meanwhile, in the Philippines, Alpha IVF has entered a strategic joint venture with two prominent fertility specialists. A flagship centre in Quezon City, Manila is underway and is expected to add 1,500 annual OPUs to the Group’s growing capacity, lifting total capacity to 9,500 OPUs annually.

With a solid 3-star ESG rating and earnings on track; with 1QFY25 core net profit already achieving 21.3% of full-year projections, Alpha IVF is well-positioned to deliver sustained shareholder value. The Group’s combination of robust domestic operations, high-margin foreign patient base, and strategic expansion into Indonesia, China, and the Philippines, solidifies its status as a regional leader in reproductive healthcare.

In summary, Alpha IVF presents a compelling case of growth at an attractive valuation, with multiple catalysts lined up across ASEAN and China. The current share price of RM0.290 offers a deep value entry point for investors with a medium- to long-term horizon.

$ALPHA / 0303 (ALPHA IVF GROUP BERHAD)