$INNO / 6262 (INNOPRISE PLANTATIONS BERHAD) – cash flow machine

Numbers from latest qr

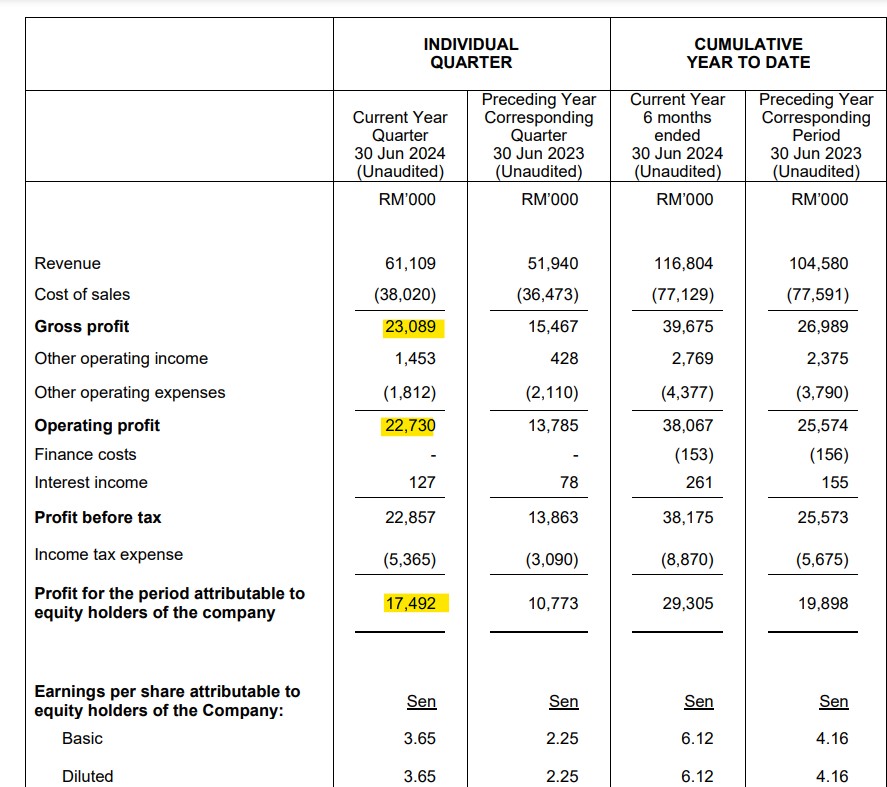

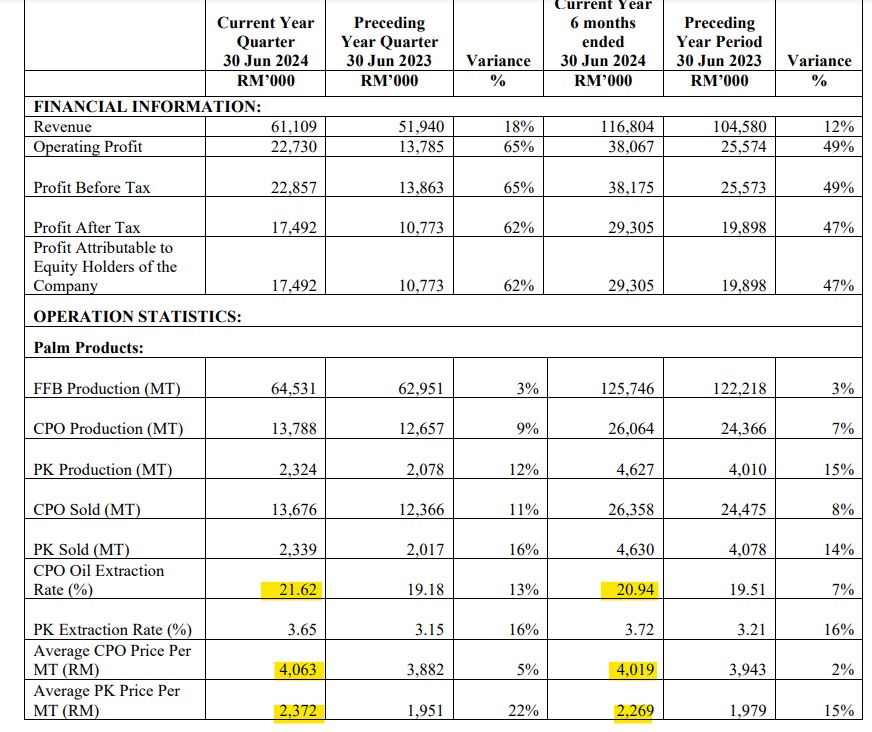

1. Operating profit 22.7m / 61.1m revenue = 37.15% opm. PAT 17.5m / 61.1m = 28% npm.

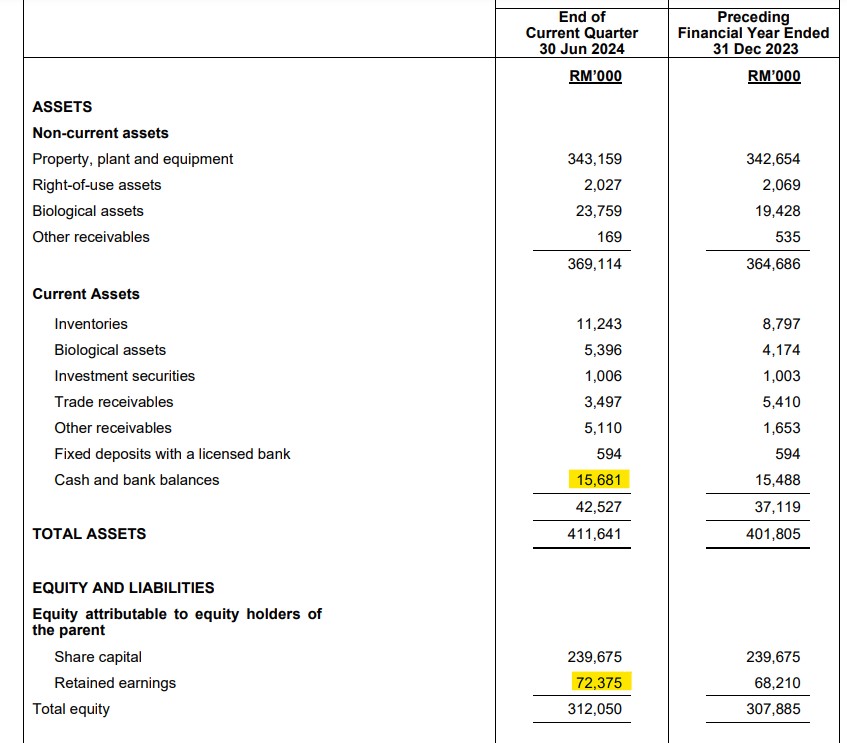

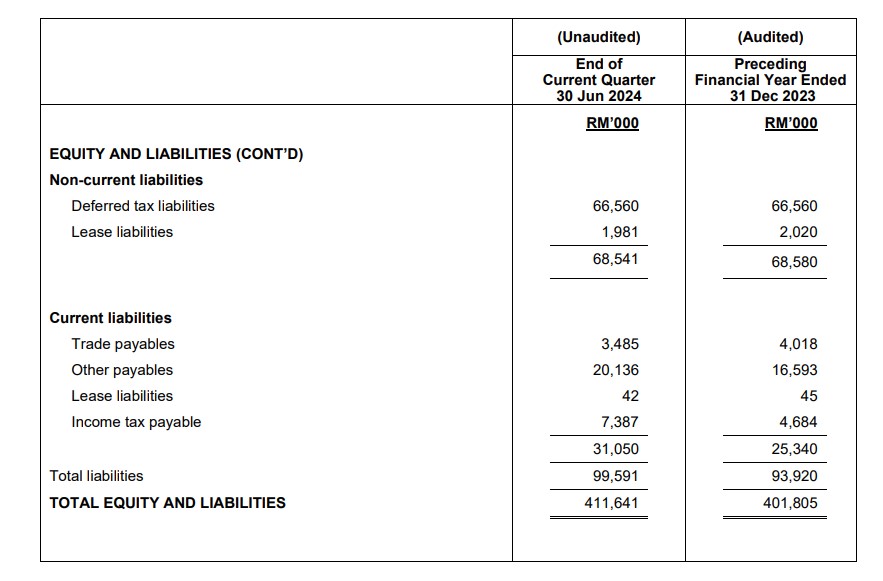

2. Net cash no debt

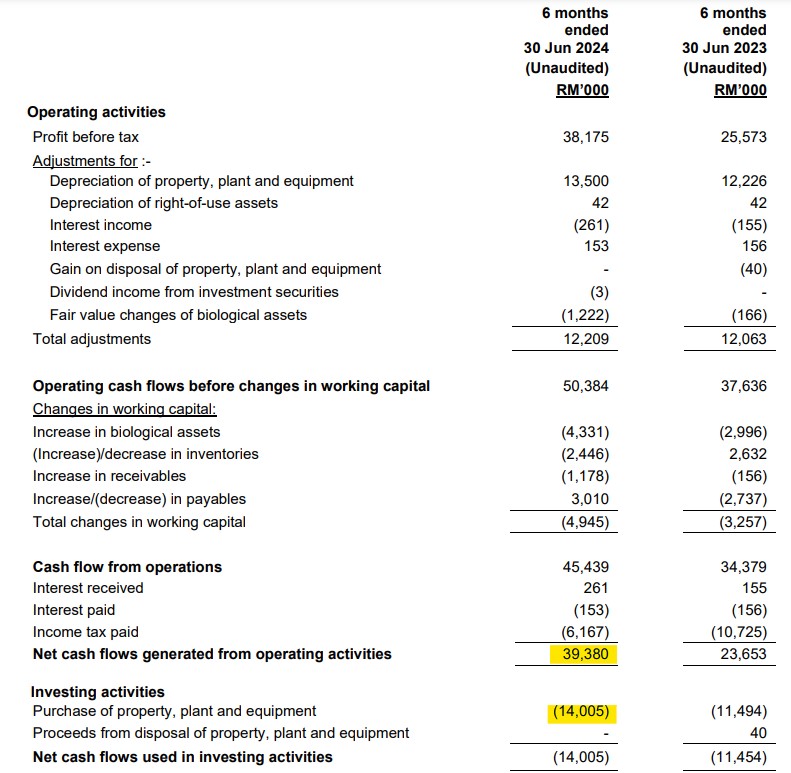

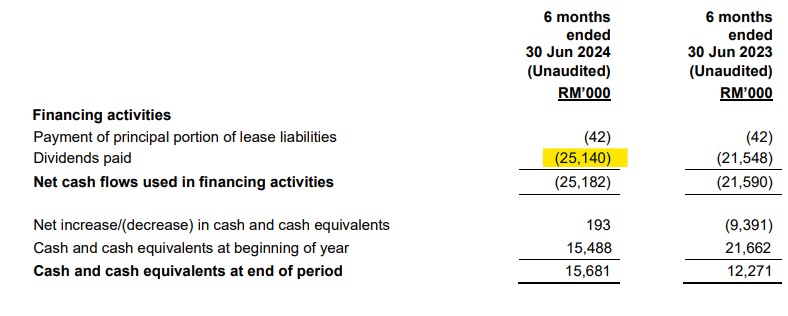

3. Nocf is 39.4m. Capex cost 14mil. FCF 25.4m. Dividend paid RM 25.1m. Dividend to FCF ratio =99%.

4. OER 21.62%.

5. ASP CPO RM 4063/mt

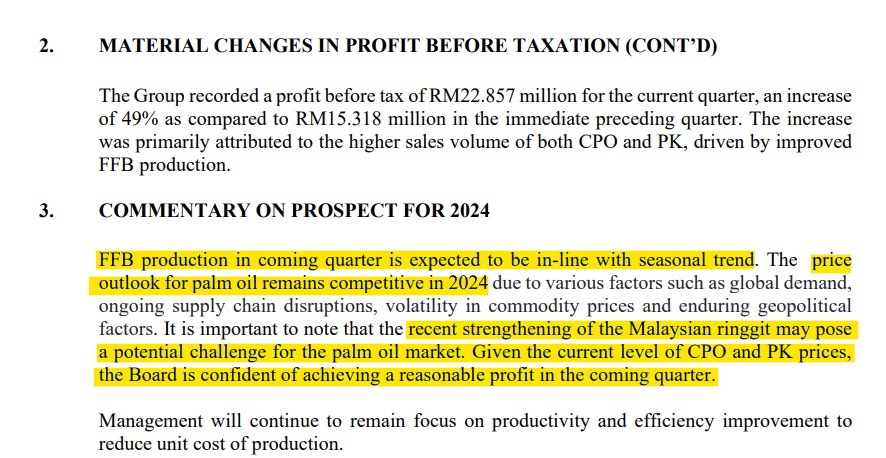

6. Expect FFB production to be in line with seasonal trend => peak season coming

7. CPO price under pressure from strengthening MYR.

8. At current CPO and PK price, management expects reasonable profit.

Ppl look at plantation company for yield, so no point using PE. Easy and lazy then use DY. More hardworking should use FCF yield is better. Inno fcf yield abt 7.5%. payout ratio over 90%. Very good dividend but upside purely depends on harvest and price of CPO. If your thesis require cpo price to go up, then I guess not so good, not conservative. Taking risk with low upside and dependent on factors out of our control. But is good case study to do. If the co can increase fcf even with cpo price flat, that will be good.

now i do this I see why which plantation counter very attractive

@terence775 @realalvinang @bursameme @littleshare @Jay888 @zhexiangxd

1/7