Here's a no brainer trading idea for you all, since I saw an interesting discussion on Cocoa Prices.

In Bursa, Teck Guan Perdana is the *only* upstream cocoa producer, as far as I know. Many others had ceased production and the cocoa production in Malaysia is now miniscule compared to a few decades ago. Then, Teck Guan being profitable shows their strong capabilities indeed.

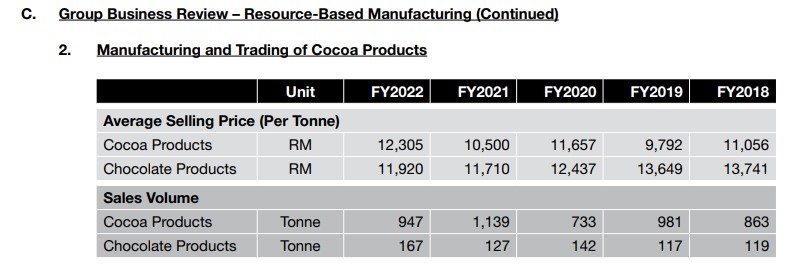

With ASP of RM 10.5k per ton, they made a segmental profit of RM 1.3m in 2021.

With ASP of 12k per ton, they made profit of RM 1.75m in 2022.

15% increase in ASP leading to 35% increase in profit.

You can clearly see the operating leverage coming into play.

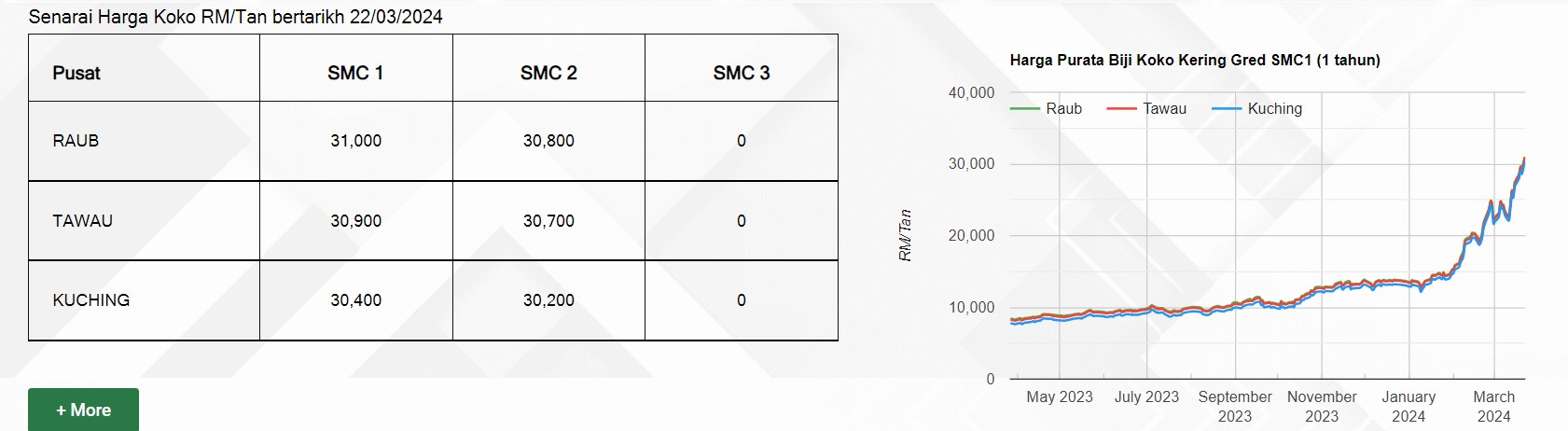

What's the ASP of cocoa now?

Here's the answer: RM 32k per ton.

How much could this segmental profit be?

In Q3 alone, when cocoa prices were roughly RM 10k per ton, they have made RM 1m in profits. This makes sense since cost of production has been dropping compared to 2022.

In the yet to be announced Q4 end of this month, the ASP was closer to RM 15k per ton.

Would RM 2m profit be possible in this quarter?

So far in the 2 months of the current quarter, cocoa prices have skyrocketed to over RM 30k per ton. I think RM 6m profit is not too far fetched.

Add on to that CPO is generally stable generating about RM 4m profit a quarter, and that CPO prices are around 15% higher compared to the previous quarter. But let's just be conservative and say CPO contributes RM 4m profit.

in 9M 2023, Teck Guan has already got a net profit of close to RM 8m.

In total, I would expect Teck Guan to have operating profit of around RM 10m, and a PBT of around RM 8m per quarter. Annualizing it means about RM 40m operating profit and RM 32m PBT, with 25% tax bringing it to a PAT of RM 24m.

Do the numbers seem too small to you?

Need I remind you that Teck Guan is only RM 70m in market cap? Funds can only watch in envy because the company is too small for them to take a position in. Unless $TECGUAN / 7439 (TECK GUAN PERDANA BERHAD), for whatever reason, climbs up 100-200%.

Icing on the cake:

1) They have resumed paying out dividends too, since their estates are all matured.

2) Rate cut bets leaves few commodity shortists and many longs.

3) Their cocoa products are exported-- weakening MYR is another benefit to them.

The QR will be announced at the end of the month. Those who know, know. It's a good time to be a farmer of non-price-controlled goods. Do your own due diligence and trade at your own risk.

1/2