$JTIASA / 4383 (JAYA TIASA HOLDINGS BHD) – 100% fully planted and in prime age, entering into cash cow mode. A potential dividend yield play in turbulent times

Plantations had been making some headlines recently, as their share prices started to move up. I’ve mentioned many times that as long as CPO is above RM 3000++, most planters will make very good money. The common argument then, is that due to “ESG” issues, plantations will forever remain “dead” as big funds will not invest into them. So how would an investor make money in the plantation sector?

**written by terence775 purely for education purposes only. This should not constitute as investment advice, and everyone should do their due diligence before making any buy or sell decisions.

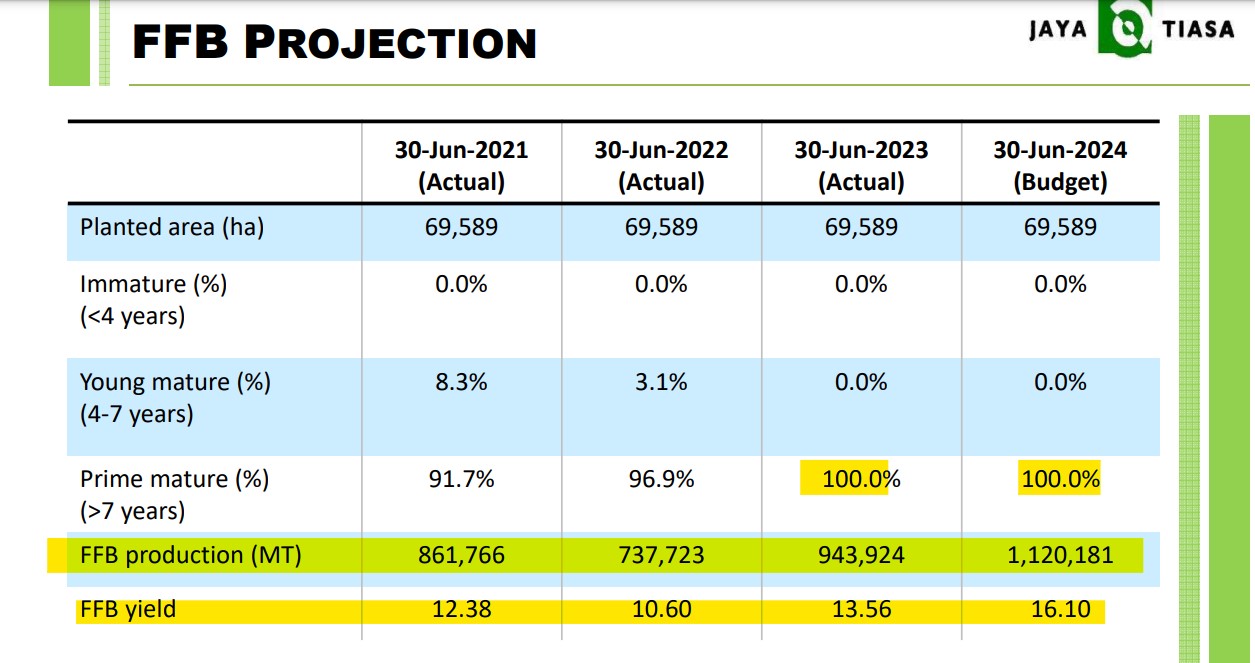

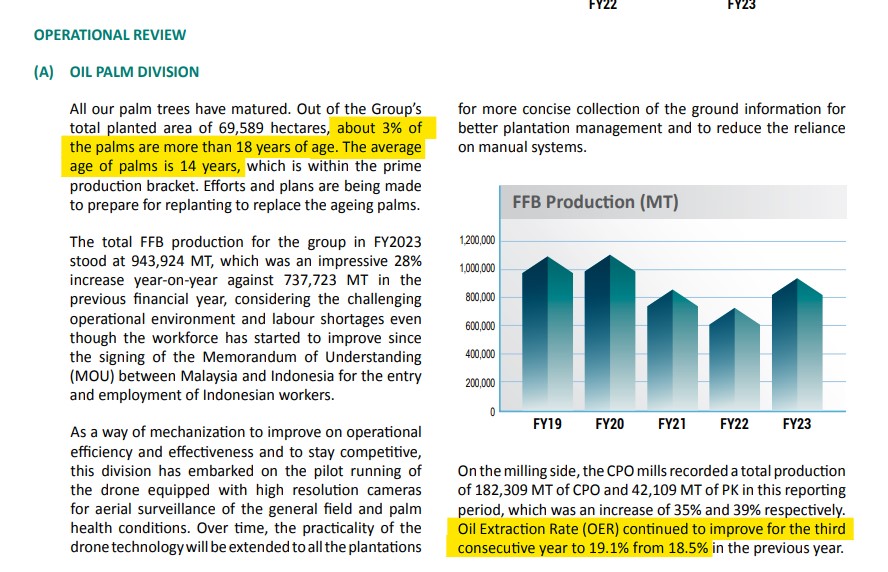

Just like how we discussed $INNO / 6262 (INNOPRISE PLANTATIONS BERHAD) back in 2021 and at one point their DY had gone above 20% (before the market reacted to it when CPO reached RM 8k per ton), JTIASA is also reaching a stage where I believe they will start to payout more dividends compared to the ~20% payout ratio they had been giving in the past. Planting efforts, which have high capex and long waiting times to bear fruit, have been mostly completed with their plantations now 100% fully planted and also 100% are prime aged palms.

Generally speaking, once palm trees have started fruiting, they will generate stable and high yields for close to 20 years of their lives before the next replanting cycle begins again. During this time, plantations will use the cash to pare down the debts taken and finally reward shareholders with the excess cash until the next cycle begins. Of course, no plantation company will have extreme cycles and they typically stagger the age of the trees. In JTIASA’s case, the avg age of their trees is 14 years old, with only 3% over 18 years. This implies that the FFB high yields should be able to last and climb for a few more years.

For macro analysis on supply/demand, which country is increasing imports, palm oil inventory level, etc etc I believe the analysts had already covered them in enough detail so if you just do some searching on the reports from bursabuzz you can get most of the information you need.

Let’s just run through a few key points and scenarios on how I would approach this:

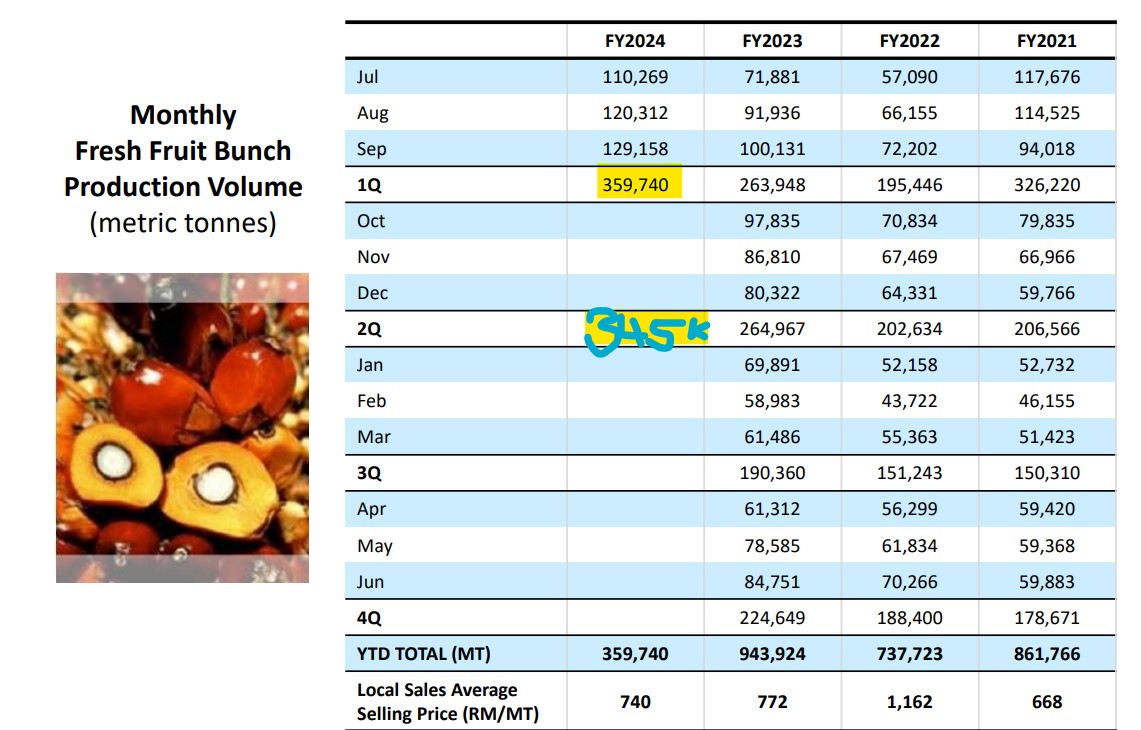

1. The management is expecting FFB production for 2024 to reach 1.1mil MT. So far, in 6 months, they have already reached about 700k MT, but bearing in mind that typically Jan-May tend to be the dry and lower production season. They do seem to be on track to hit their target.

2. The aforementioned low production period (experienced by all plantations) theoretically can support CPO price from dropping too much.

3. CPO, as a commodity, is obviously highly cyclical. However, unlike other industrial commodities like steels and metals, CPO is heavily used in the production of necessities (food, soap, cosmetics, and so on). Therefore, even in a recession, demand for CPO should be quite steady. It’s worth noting that JTIASA has hardly any hedging, so their sales will be mostly done on spot.

4. Also unlike other commodities, it’s not that easy to increase supply due to various reasons; approvals, clearing land, and a few years of time for the trees to grow.

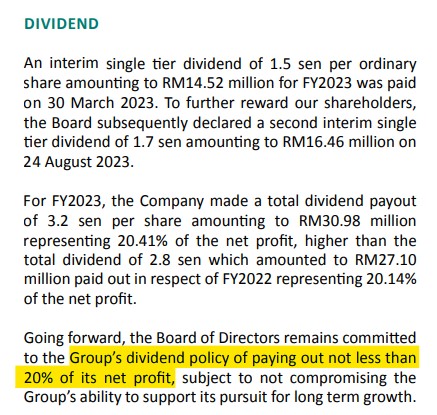

5. Historically, JTIASA has always paid out around ~20% of PAT to shareholders. Meanwhile, the remaining cash would be used to pare down debts or fund CAPEX.

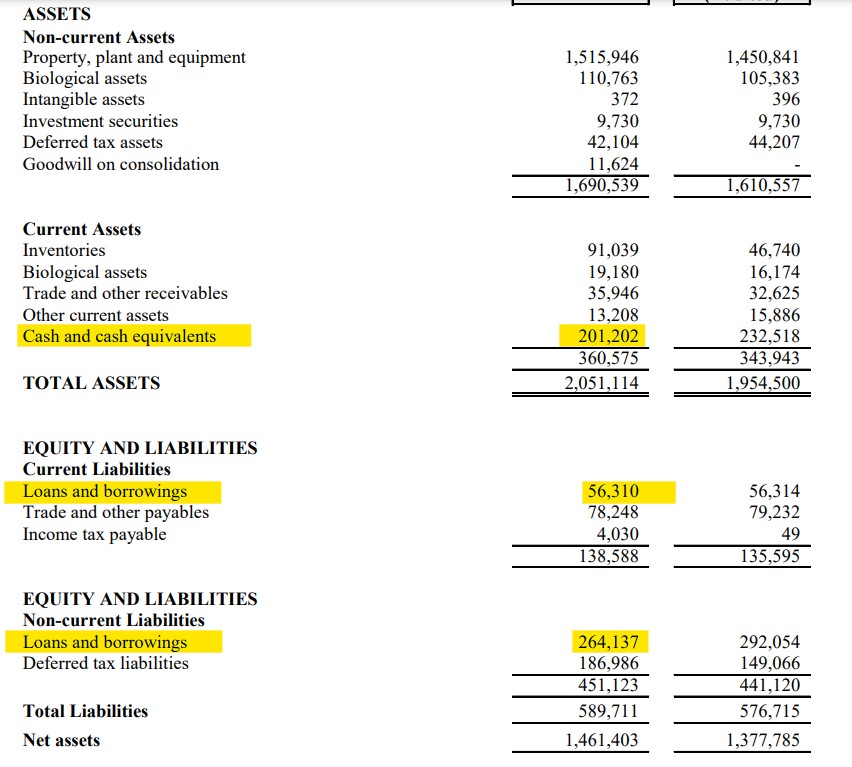

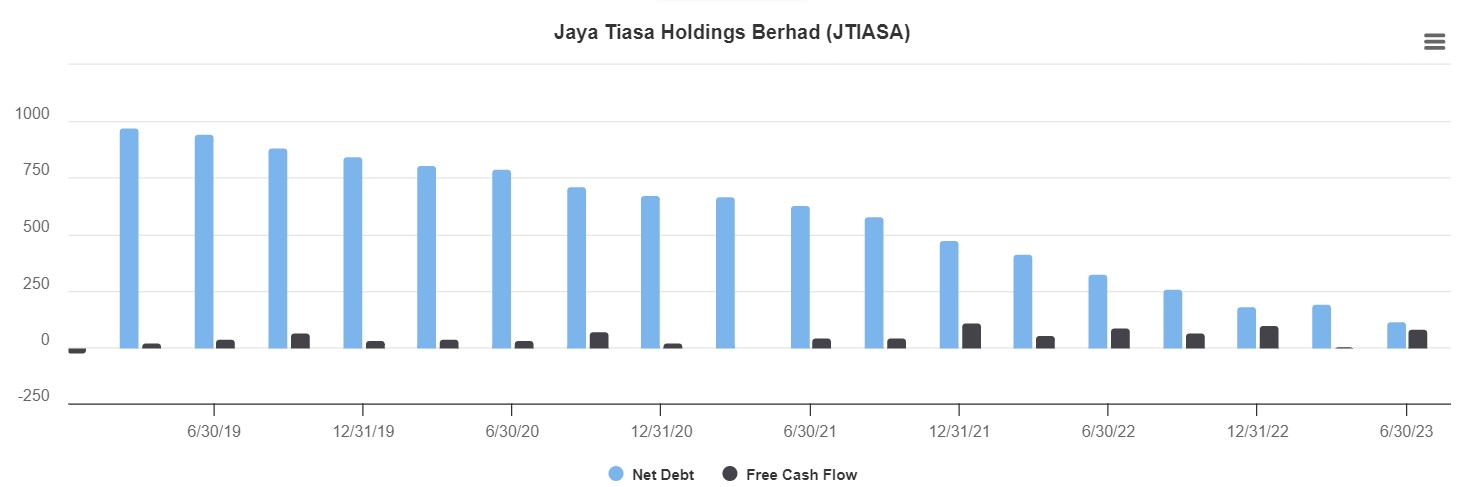

6. Currently, their borrowings have dropped to around RM 310mil only (from billions previously), with cash on hand of around RM 200mil, making them effectively net debt of about RM 110mil.

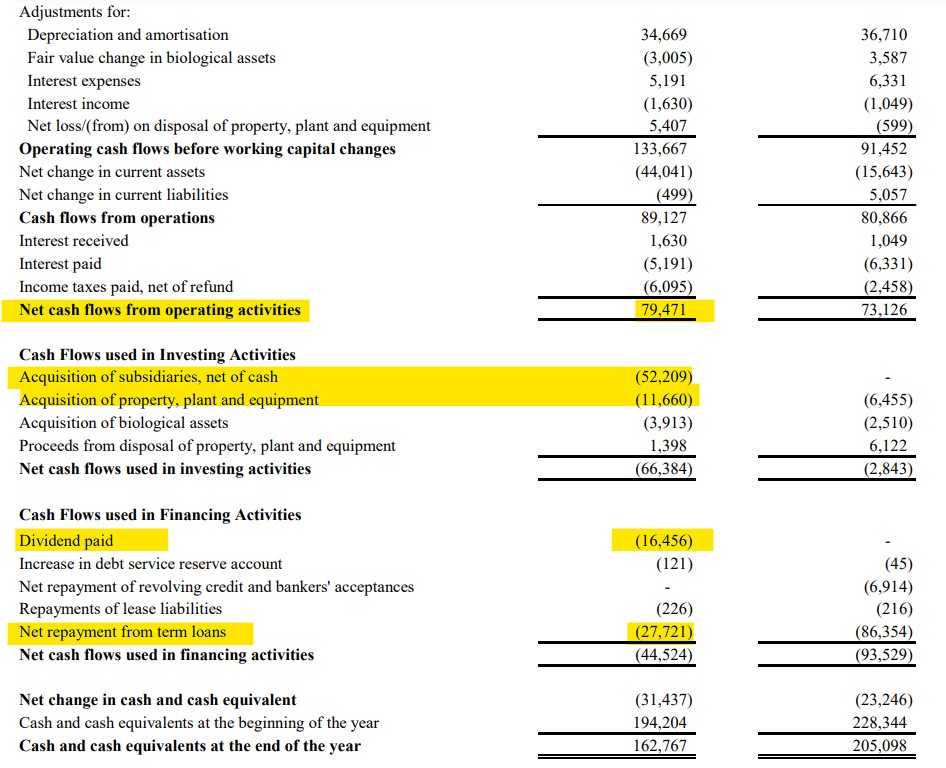

7. Net operating cash flow is around RM 80mil a quarter, or about RM 320mil a year if we annualize it. Aside from the acquisition they made recently amounting to RM 52mil (to acquire another estate), the CAPEX spent was RM 11mil this quarter, giving FCF of approx. RM 69mil. Of which, RM 28 mil was used to pare down debts and RM 16.5mil was paid out as dividends.

8. Their NOCF could basically pay off all their remaining debt this year if they decide to do so. This will also help in reducing finance costs.

9. With not many reinvestment opportunities and debts almost cleared off, I think it is reasonable to assume they will start paying out more dividends.

10. Recall that in INNO’s case, the payout ratio went as high as over 100% of net profit being distributed (basically all operating cash flow).

What actionable insights can we take from here?

Let’s do a basic analysis of one possible scenario:

Assuming CPO price remains stable, and annualizing the Q1 performance…

1. We are looking at approximately ~RM 240-250mil PAT this year, EPS of around 28sen, and EBITDA of about RM 440mil. Of course, you should conduct a sensitivity analysis to determine the range of potential profit and cash flow numbers being reported, and also taking into account cost of fertilizers which are commodities too.

2. You can easily check production/harvests numbers as they are reported every month. It will be worthwhile to create your own excel sheet to track production vs ASP and make adjustments as the data becomes available.

3. If JTIASA pays out 20% of PAT, the dividend would be around 5.8sen. At current price of around RM 1.2, that would be a DY of around 4.5+%.

4. If they pay out 50%, it would be around 14sen...

5. If they pay out 100%, it would be 28sen...

6. And if they pay out their whole operating cash flow (earnings before D&A basically, which are non-cash items), that would be closer to around 30+% yield.

The above would constitute one scenario. I would repeat it by changing various parameters, mainly CPO price and yields, and evaluating it again to come up with a range of results. What are appropriate assumptions? What should be discounted? Having a feel for this will help you come up with reasonable calculations for your valuation exercise. You can use the same methodology to examine all the other plantation companies and see if any others can be a good deal too.

Main risks I can think of:

1. Volatility of CPO price.

2. Unpredictable weather leading to lower output than expected either by drought or major flooding.

3. Timber and logging business are loss making for now—this could be an upside if they manage to turn it around but generally it’s a small % of total revenues. It’s worth mentioning that timber are generally priced in USD, and both USD and timber prices have been climbing in the past year.

4. Share price movement is, of course, subject to market forces.

5. Unreliable track record of the company—no guarantees that the management will pay out more dividends and they could just keep the money in bank or use it to make acquisitions.

Personal thoughts:

I think this exercise is worth doing for those who are interested in dividend income. Jtiasa is one of those plantation stocks that is in a sweet spot right now, something like an inflection point, over the years of their capex cycle and is probably looking to return profit to shareholders, which are majority owned by the founding family. Compared to their peers, they are cheaper, which could be due to either lack of market awareness or discounts due to the less than stellar track record of the company. Good luck!

Did I miss anything? How would you improve this analysis? Let me know!

1/7