$TMCLIFE / 0101 (TMC LIFE SCIENCES BERHAD) – Award Winning Healthcare Provider, Malaysian Book of Records holder, and one of the leading Fertility centres in SEA with Just-Completed Expansion and seeing Stronger Numbers being Reported

Preamble:

I guess most people would have heard of TMCLIFE already in some way or another. In Malaysia, TMCLIFE is a 70% owned subsidiary of Thomson Medical in Singapore via Sasteria Pte Ltd. and they operate Thomson Hospital in Kota Damansara (THKD) as well as a number of fertility clinics around Selangor, Penang, Ipoh and JB. THKD was in operation since 2008, and they have been growing over time. Most recently, they did a major expansion by increasing the capacity by around 50%, from ~200beds in 2022 to 314 beds now (I believe it was completed sometime around April 23’). As usual with most expansions, the numbers generally take time to come after “commissioning” due to various real world issues including demand catch up, teething issues, onboarding personnel, etc. THKD is still in the midst of expansion, with their end goal being ~500+ beds at THKD and the new Thomson Iskandar Medical Hub in Johor Bahru “within 12-24 months after the Rapid Transit System at Bukit Chagar is fully operational”. The land is already there at Vantage Bay, and I understand approvals have already been gotten. However, while preliminary construction has started, construction proper has yet to begin. It is proposed to be of similar size to THKD sporting ~500beds at max capacity however it seems to be a story of 2027- and beyond, which may not necessarily be a bad thing.

Anyway, as pointed out by @boncos here: https://cutt.ly/SwEBVPxX , the numbers have indeed started to flow in however the share price has yet to particularly move much. This could be due to any number of reasons such as the macro environment investors find themselves in amongst other things.

For now, they had just released their Annual Report, so let’s go through some interesting points I found.

*written by terence775, purely for sharing purposes and not to be taken as investment advice in any way*

TMCLIFE AR 2023:

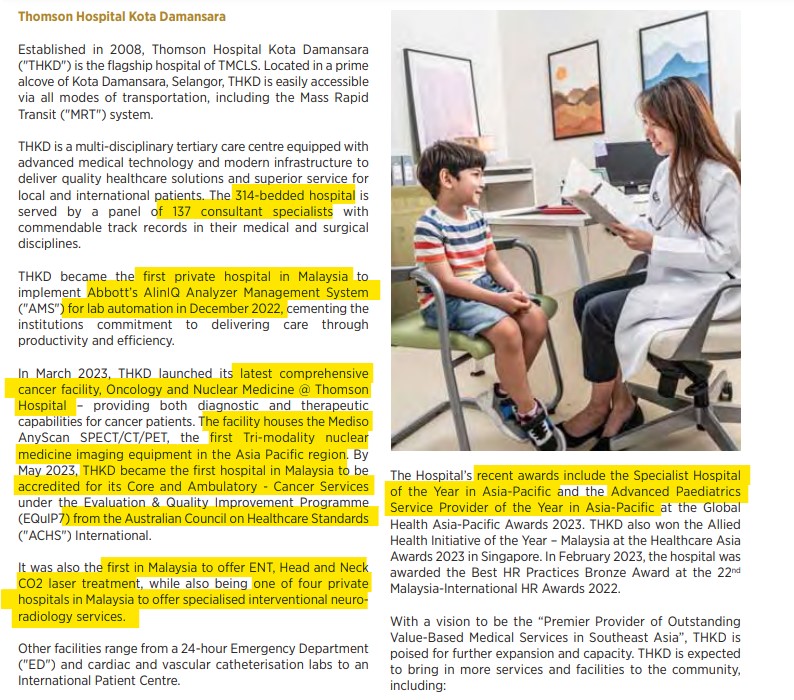

1. Straightaway, they don’t hesitate to tell you how many “firsts” THKD has.

a. First Private Hospital in Malaysia to implement Abbott’s AlinIQ AMS for automation in laboratories. According to Abbott’s website, their AMS system helps improve turnaround time of analytics by about 60%. This is expected to improve productivity, accuracy, versatility and uptime of their lab operations.

b. In the scene of Oncology and Nuclear Medicine, TMCLIFE houses the first Tri-modality nuclear medicine imaging equipment in ASIAPAC.

c. They are also the first hospital in Malaysia to be accredited for its Core and Ambulatory – Cancer Services under EQuIP7 from Australia (ACHS) International.

d. First in Malaysia to offer ENT, Head and Neck CO2 laser treatment, and one of four private hospitals in Malaysia to offer IV Neuroradiology services.

e. THKD also recorded their first Kasai surgery and first Thymoma surgery this year, after expanding their services to include palliative care, ophthalmology, and vitreoretinal, rheymatology, paediatric anesthesiology and vascular surgery.

2. They also have been awarded a bunch of titles such as:

a. Specialist Hospital of the Year ASIAPAC

b. Advanced Paeds Service Provider of the Year ASIAPAC

c. Allied Health Initiative of the Year – Malaysia

d. Innovative Technology in Healthcare Sector for Fertility Treatments in ASEAN

e. Gastroenterology Service Provider of the Year ASIAPAC

3. TMC Fertility runs one of the largest IVF labs in SEA, and one of the first in MY to be certified by RTAC, Australia.

4. TMC Fertility is also the Malaysian Book of Records holder for Highest Number of IVF Babies produced by a single IVF practice.

5. TMC Care, their pharmacy arm, operates a retail outlet as well as an online store.

6. They also have Thomson Traditional Chinese Medicine (TCM), which operates both physically as a clinic, as well as online. This TCM segment has won the TCM Center of the Year ASIAPAC awards for 2022 and 2023 respectively.

7. Due to deferred tax credits, net profit for 2023 declined 5% compared to 2022. Operationally speaking, their net profit would have increased by 36% excluding the deferred tax credits.

8. CAPEX allocation is RM 21.8mil, of which RM 13.8mil is for expansion. It seems like the major CAPEX cycle has ended for now, after spending more than RM 250mil in CAPEX in the past few years.

9. Another Malaysian Book of Records entry—First Hospital Alliance with Tertiary Educational Institution. This aims to improve the healthcare landscape by having cooperation with universities. At the same time, they could potentially attracted top talents to work for them.

10. THKD plans to continue to focus on their niche as a children and women healthcare hub.

11. An interesting business model is their collaboration on the medical tourism front, whereby they partner up with travel and tour agencies to offer holiday and retreat packages while receiving treatment at TMC Fertility via Medical Referral Agents. This targets international customers which bodes well as these groups of people tend to have more to spend…

12. Looking at the shareholder list, we can see that TMCLIFE has very low float, with the top 3 holding 84.35% and the top 10 holding 89.63% of the company. Major shareholders are Sasteria (M) Pte Ltd, which is a subsidiary of Thomson medical Singapore; and as pointed out by @realalvinang, the Duli Yang Amat Mulia Tunku Ismail Ibni Sultan Ibrahim of Johor holds 7.64%. UOBKH nominees (asing) holds 6.58%. This is a consolidated nominee holdings through UOBKH, and probably their Singapore clients so it’s likely not to be a singular entity.

13. Other interesting names on the top 10 are Credit Suisse AG (their numbers have been up and down over the years), Lembaga Tabung Amanah Warisan Negeri Terengganu (have been increasing over the few years), Philip Capital (new top 10).

Financials:

Revenue and PBT have been growing steadily over the past 10 years, with revenue and PBT CAGR of 15.3% and 22.2% over 10 years. This is definitely commendable. They have also been paying dividends, albeit with a low-ish payout ratio of around <15%, but nevertheless in line with the growing profits, the dividend paid out have also increased by 9.4% CAGR over the past 10 years.

Balance sheet is healthy with minor net debt position, bulk of it non-current. I don’t expect them to run into any liquidity crises or have any need to raise funds from the market.

Thought on future Dividends:

Recently, they have declared a special dividend and also their highest payout yet at 0.84sen (pending approval at the AGM on Thursday!), which is equal to a payout ratio of around ~37%. This comes after huge CAPEX spending over the past 3 years for expansion. With major CAPEX already having been spent, I think we are set for a few years of higher payouts before the next expansion cycle (probably for Thomson Iskandar).

Valuation:

Hospitals and healthcare related counters are generally always at a premium; and TMCLIFE has a TTM PE of ~26x while their RoE is only 4.6%. That being said, I’ve explained before about business cycles and financial valuation, so it’s good to draw your own estimations based on your own projections. I believe stronger numbers are incoming; but you will have to do your due diligence for that.

Competitors and Peers

Hospitals and Medical Centres: IHH, KPJ, CENGILD, LYC

The other hospital players are all more or less having around the same kind of premium as TMC, with the exception of LYC, focusing on confinement and postnatal care, being continually loss making for years. KPJ and IHH are both much larger than TMCLIFE. IHH has added risk of geopolitics with exposure in Turkiye, India, Europe, China and so on.

Closing thoughts:

Looking at their direct competitors, most of them are expanding too. Does this make the hospital industry a saturated one? Will there be more supply than demand? Well, judging from the number of beds compared to the population as a whole, Malaysia is still quite within the average range with ~1.8 beds per 1000 people. There are plenty of countries with higher number of beds per 1k people than us, whether with higher per capita GDP or lower. This makes me think that the industry is still quite within equilibrium and, especially for TMCLIFE which operates in the more upmarket segment, can probably maintain their pricing power and margins.

Whilst the world is threading on unsteady ground, healthcare will always play an important role and shouldn’t lack demand. We shall see how the numbers continue to flow in in the coming months.

tagging people who might be interested in TMCLIFE

@tapdance @realalvinang @boncos @zhexiangxd @jay888 @MICHAELWILBERT1 @Travellingme @elenov

1/10