$SAMCHEM / 5147 (SAMCHEM HOLDINGS BERHAD) ‘s latest QR for Q2FY023 is out.

Samchem continues to remain profitable albeit lower revenue and net profit QoQ and YoY.

# Comparing current quarter Q2FY2023 with preceding year corresponding quarter Q2FY2022:

- Rev dropped 25% to RM 276.23 mil due to drop in ASP and sale vol.

- Cost of Sales/Rev also inched up a bit from 87% to 89%.

- Selling & Distribution expenses increased by 14% despite dropping rev.

- Other operating expenses did reduce by 96% to RM 69 mil.

- PBT decreased by 70% to RM 7.89 mil due to lower sales vol and margin compression.

- PAT dived 72% to RM 6 mil.

- Net profit margin contracted from 5% to 2%.

- EPS decreased from 3.35 sen to 0.99 sen.

- OCF turned positive to RM 8.4 mil from previously negative RM 11.64 mil.

- Geographical revenue segment: Malaysia (47%), Vietnam (45%), Indonesia (6%), Singapore (2%). The drop in revenue yoy in terms of percentage wise, Indonesia leads the pack (- 33%), followed by Malaysia (-27%), Vietnam (-21%) and Singapore (-24%).

- Geographical PBT segment: Malaysia (67%), Vietnam (25%), Indonesia (3%), Singapore (5%). The drop in PBT yoy in terms of percentage wise, Indonesia again leads the pack (-80%), followed by Vietnam (-76%), Malaysia (-68%) and Singapore (-22%).

- A second interim dividend of 0.5 sen per ordinary share was declared.

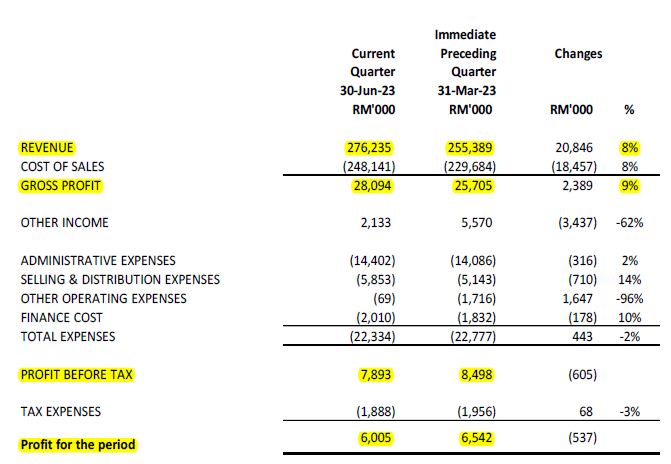

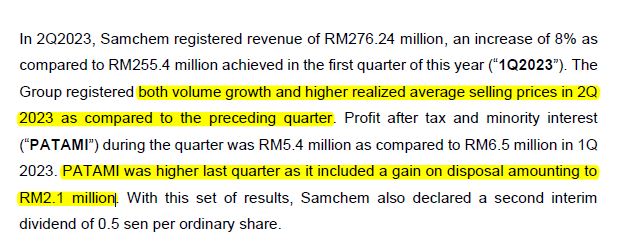

# Comparing current quarter Q2FY2023 with immediate preceding quarter Q1FY2023:

- Rev increased by 8% to RM 276.23 mil due to vol growth and higher ASP.

- Cost of Sales/Rev remained steady at around 89%.

- Total expenses remained relatively the same with only a 2% drop.

- PBT decreased by 7% to RM 7.89 mil due to a one off disposal gain of a factory of RM 2.1 mil in the preceding quarter.

- PAT also decreased by 815 to RM 6 mil.

- Net Profit Margin dwindled to 2% from 2.6% previously.

- Malaysia remained the largest rev contributor, followed by Viet, Indo and Singapore.

# Prospects:

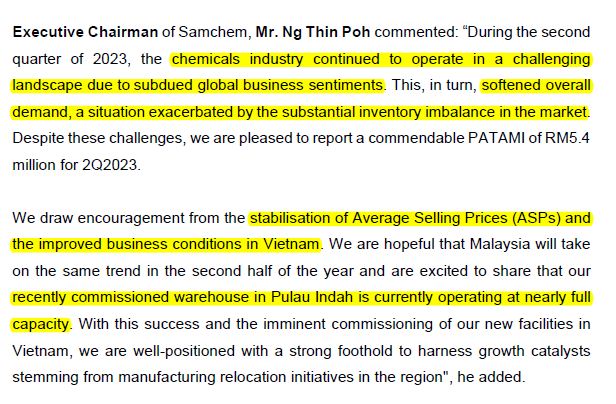

- Mr. Ng Thin Poh (Executive Chairman) stated that the chemicals industry continued to operate in a challenging landscape due to subdued global biz sentiments.

- This led to softened overall demand, a situation exacerbated by the substantial inventory imbalance in the market.

- Mr. Ng also added that the Group drew encouragement from the stabilization of ASP and improved biz conditions in Vietnam and they are hopeful that Malaysia will take on the same trend in 2H2023.

- The recently commissioned warehouse in Pulau Indah is currently operating at near full capacity.

- Lastly, the Groups are well-positioned with a strong foothold to harness growth catalyst stemming from manufacturing relocation initiatives in the region given the success and imminent commissioning of their new facilities in Vietnam.

1/6